Tenant’s democracy in Denmark

Main objectives of the project

In numerous European countries, social housing landlords have established mechanisms for tenant involvement in governance, with Denmark leading the forefront in this domain, where it has evolved into what is commonly referred to as "tenant democracy." Within this system, tenants of housing associations possess the ability to wield substantial influence over estate management.

Date

Stakeholders

- Promotor: BL- Danish Federation of Non-Profit Housing

Location

Country/Region: Denmark

Description

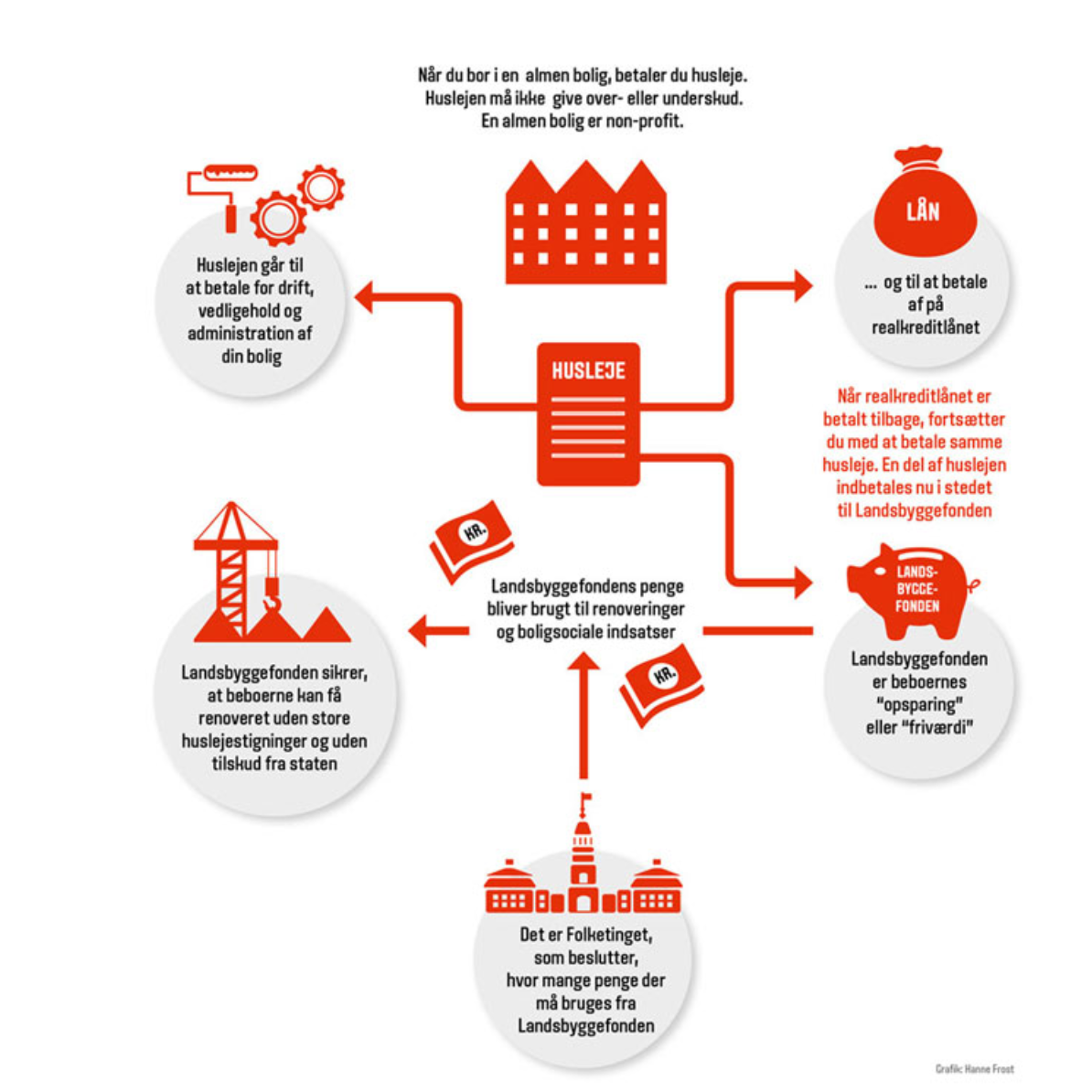

Denmark boasts a rich history of equitable housing policies spanning over a century. In 1919, through broad political consensus, Denmark pioneered a national public social housing system accessible to all. Unlike public housing models elsewhere, social housing in Denmark is not confined to low-income households but is open to all residents. Nonprofit housing organizations, where tenants are associates, develop and own the buildings, while residents actively shape their living conditions through a system of tenant democracy. Regulated extensively under Danish welfare policy, nonprofit housing development encompasses stringent controls over financing, design, construction, and management, including waiting lists for housing units. Danish law allows each municipality to allocate up to 25% of its social housing stock for marginalized communities such as refugees, the unemployed, and people with disabilities. Social housing comprises approximately 20% of Copenhagen's housing stock, while market-rate rentals and private co-ops constitute 43% and another significant portion, respectively.

A cornerstone of tenant democracy in Denmark lies in tenant boards. Each housing estate annually elects its tenant board, which subsequently forms part of a larger assembly. This assembly convenes annually to elect a board, approve budgets and rents, determine maintenance and renovation projects, and establish local rules. Tenants hold substantial power in decision-making, with the board having the final say, even on major renovations. Disputes are resolved through municipal assistance mechanisms when necessary, ensuring equitable outcomes. While tenants maintain the majority on the organization's board, municipal representatives often occupy seats as well. Thus, participatory methods, reinforcing local power and horizontal governance are the main features of the model.

To further empower tenant boards, housing associations offer various tools and resources. These include dedicated web portals for board members and a range of courses, such as an annual weekend seminar for local housing company chairpersons and chairwomen, along with meetings held in local settings with high-level executives from the housing associations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}